Regression analysis -- multiple regression

Introduce the statistics in multiple regression analysis

- Total observed value

- Total independent variable

- Freedom

: return degrees of freedom

: return degrees of freedom , residual degrees of freedom

, residual degrees of freedom

- Sum of total square of SST

- Sum of squares of SSR regression

- Sum of squares of SSE residuals

- MSR mean square regression

- MSE mean square residual

- Determination coefficient R ﹣ square

- Adjusted? R? Square

- Multiple? R

- Standard error of estimation

- F-test statistics

- Standard error of sampling distribution of regression coefficient

- t-test statistics of regression coefficients

- Confidence interval of each regression coefficient

- log likelihood

- AIC guidelines

- BIC guidelines

Case analysis and python practice

# Import related packages import pandas as pd import numpy as np import math import scipy import matplotlib.pyplot as plt from scipy.stats import t

# Building data

columns = {'A':"Branch number", 'B':"Non-performing Loan(Billion yuan)", 'C':"Loan balance(Billion yuan)", 'D':"Accumulated loans receivable(Billion yuan)", 'E':"Number of loan items", 'F':"Fixed assets investment(Billion yuan)"}

data={"A":[1,2,3,4,5,6,7,8,9,10,11,12,13,14,15,16,17,18,19,20,21,22,23,24,25],

"B":[0.9,1.1,4.8,3.2,7.8,2.7,1.6,12.5,1.0,2.6,0.3,4.0,0.8,3.5,10.2,3.0,0.2,0.4,1.0,6.8,11.6,1.6,1.2,7.2,3.2],

"C":[67.3,111.3,173.0,80.8,199.7,16.2,107.4,185.4,96.1,72.8,64.2,132.2,58.6,174.6,263.5,79.3,14.8,73.5,24.7,139.4,368.2,95.7,109.6,196.2,102.2],

"D":[6.8,19.8,7.7,7.2,16.5,2.2,10.7,27.1,1.7,9.1,2.1,11.2,6.0,12.7,15.6,8.9,0,5.9,5.0,7.2,16.8,3.8,10.3,15.8,12.0],

"E":[5,16,17,10,19,1,17,18,10,14,11,23,14,26,34,15,2,11,4,28,32,10,14,16,10],

"F":[51.9,90.9,73.7,14.5,63.2,2.2,20.2,43.8,55.9,64.3,42.7,76.7,22.8,117.1,146.7,29.9,42.1,25.3,13.4,64.3,163.9,44.5,67.9,39.7,97.1]

}

df = pd.DataFrame(data)

X = df[["C", "D", "E", "F"]]

Y = df[["B"]]# Building multiple linear regression model from sklearn.linear_model import LinearRegression lreg = LinearRegression() lreg.fit(X, Y) x = X y_pred = lreg.predict(X) y_true = np.array(Y).reshape(-1,1) coef = lreg.coef_[0] intercept = lreg.intercept_[0]

# Custom function

def log_like(y_true, y_pred):

"""

y_true: True value

y_pred: predicted value

"""

sig = np.sqrt(sum((y_true - y_pred)**2)[0] / len(y_pred)) # Residual standard deviation δ

y_sig = np.exp(-(y_true - y_pred) ** 2 / (2 * sig ** 2)) / (math.sqrt(2 * math.pi) * sig)

loglik = sum(np.log(y_sig))

return loglik

def param_var(x):

"""

x:Only independent variable wide table

"""

n = len(x)

beta0 = np.ones((n,1))

df_to_matrix = x.as_matrix()

concat_matrix = np.hstack((beta0, df_to_matrix)) # Matrix merging

transpose_matrix = np.transpose(concat_matrix) # Matrix transposition

dot_matrix = np.dot(transpose_matrix, concat_matrix) # (X.T X)^(-1)

inv_matrix = np.linalg.inv(dot_matrix) # Find (X.T X)^(-1) inverse matrix

diag = np.diag(inv_matrix) # Obtain the diagonal of the matrix, i.e. the variance of each parameter

return diag

def param_test_stat(x, Se, intercept, coef, alpha=0.05):

n = len(x)

k = len(x.columns)

beta_array = param_var(x)

beta_k = beta_array.shape[0]

coef = [intercept] + list(coef)

std_err = []

t_Stat = []

P_value = []

t_intv = []

coefLower = []

coefupper = []

for i in range(beta_k):

se_belta = np.sqrt(Se**2 * beta_array[i]) # Sampling standard error of regression coefficient

t = coef[i] / se_belta # T statistic used to test regression coefficient, i.e. test statistic t

p_value = scipy.stats.t.sf(np.abs(t), n-k-1)*2 # P value used to test regression coefficient

t_score = scipy.stats.t.isf(alpha/2, df = n-k-1) # t critical value

coef_lower = coef[i] - t_score * se_belta # Lower confidence interval limit of regression coefficient (slope)

coef_upper = coef[i] + t_score * se_belta # Upper limit of confidence interval of regression coefficient (slope)

std_err.append(round(se_belta, 3))

t_Stat.append(round(t,3))

P_value.append(round(p_value,3))

t_intv.append(round(t_score,3))

coefLower.append(round(coef_lower,3))

coefupper.append(round(coef_upper,3))

dict_ = {"coefficients":list(map(lambda x:round(x, 4), coef)),

'std_err':std_err,

't_Stat':t_Stat,

'P_value':P_value,

't critical value':t_intv,

'Lower_95%':coefLower,

'Upper_95%':coefupper}

index = ["intercept"] + list(x.columns)

stat = pd.DataFrame(dict_, index=index)

return stat# Custom function (calculate and output statistics of regression analysis)

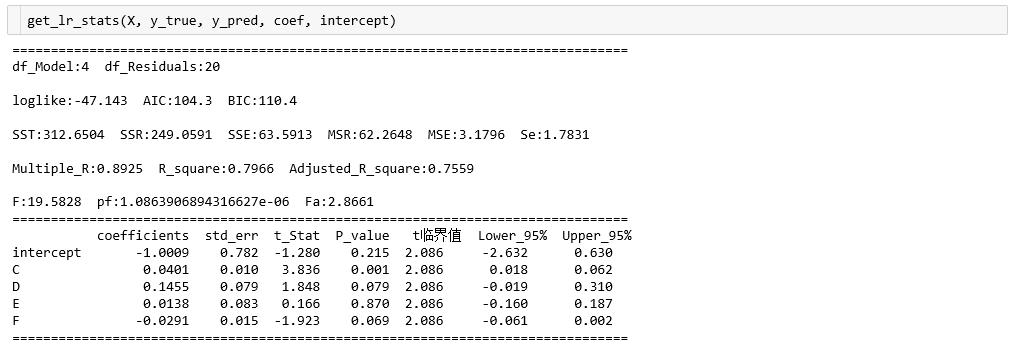

def get_lr_stats(x, y_true, y_pred, coef, intercept, alpha=0.05):

n = len(x)

k = len(x.columns)

ssr = sum((y_pred - np.mean(y_true))**2)[0] # Regression square sum SSR

sse = sum((y_true - y_pred)**2)[0] # Sum of squared residuals SSE

sst = ssr + sse # Total square sum SST

msr = ssr / k # Mean square regression MSR

mse = sse / (n-k-1) # Mean square residual MSE

R_square = ssr / sst # Determination coefficient R^2

Adjusted_R_square = 1-(1-R_square)*((n-1) / (n-k-1)) # Determination coefficient of adjustment

Multiple_R = np.sqrt(R_square) # Complex correlation coefficient

Se = np.sqrt(sse/(n - k - 1)) # Standard error of estimation

loglike = log_like(y_true, y_pred)[0]

AIC = 2*(k+1) - 2 * loglike # (k+1) represents k regression parameters or coefficients and 1 intercept parameter

BIC = -2*loglike + (k+1)*np.log(n)

# Significance test of linear relationship

F = (ssr / k) / (sse / ( n - k - 1 )) # Test statistic F (test of linear relationship)

pf = scipy.stats.f.sf(F, k, n-k-1) # Significance F for test, i.e. significance F

Fa = scipy.stats.f.isf(alpha, dfn=k, dfd=n-k-1) # F critical value

# Significance test of regression coefficient

stat = param_test_stat(x, Se, intercept, coef, alpha=alpha)

# Output statistics of regression analysis

print('='*80)

print('df_Model:{} df_Residuals:{}'.format(k, n-k-1), '\n')

print('loglike:{} AIC:{} BIC:{}'.format(round(loglike,3), round(AIC,1), round(BIC,1)), '\n')

print('SST:{} SSR:{} SSE:{} MSR:{} MSE:{} Se:{}'.format(round(sst,4),

round(ssr,4),

round(sse,4),

round(msr,4),

round(mse,4),

round(Se,4)), '\n')

print('Multiple_R:{} R_square:{} Adjusted_R_square:{}'.format(round(Multiple_R,4),

round(R_square,4),

round(Adjusted_R_square,4)), '\n')

print('F:{} pf:{} Fa:{}'.format(round(F,4), pf, round(Fa,4)))

print('='*80)

print(stat)

print('='*80)

return 0The output results are as follows:

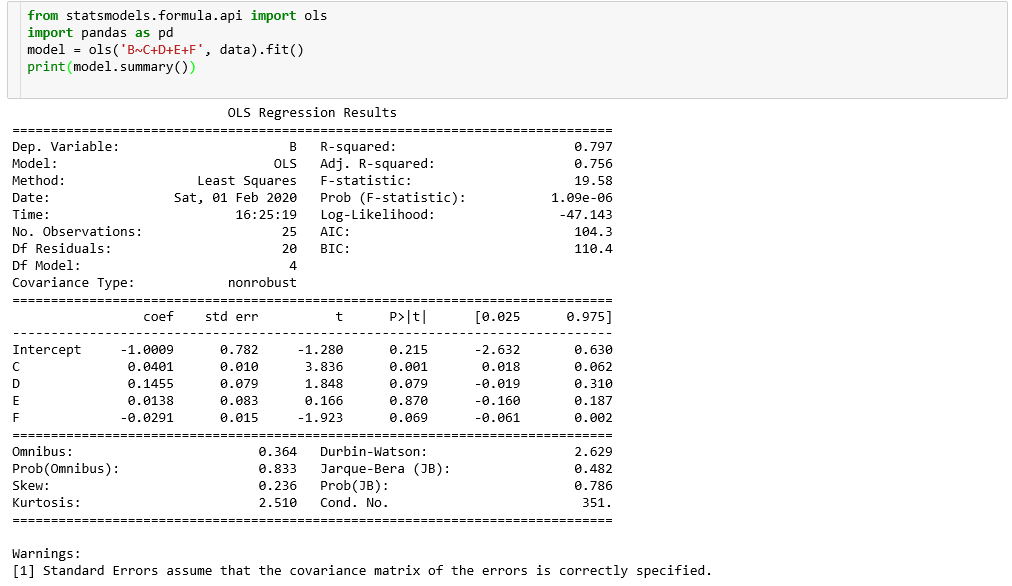

Compared with ols results under statsmodels: