Original link: http://tecdat.cn/?p=24498

In this example, we consider Markov transformation stochastic volatility model.

statistical model

Give Way  Are dependent variables and

Are dependent variables and  Unobserved log volatility The stochastic volatility model is defined as follows

Unobserved log volatility The stochastic volatility model is defined as follows

Zone variable  Following a two-state Markov process with transition probability

Following a two-state Markov process with transition probability

Represents the normal distribution of the mean

Represents the normal distribution of the mean  And variance

And variance  .

.

BUGS language statistical model

Contents of file "ssv.bug":

file = 'ssv.bug'; % BUGS Model file name

model

{

x\[1\] ~ dnorm(mm\[1\], 1/sig^2)

y\[1\] ~ dnorm(0, exp(-x\[1\]))

for (t in 2:tmax)

{

c\[t\] ~ dcat(ifelse(c\[t-1\]==1, pi\[1,\], pi\[2,\]))

mm\[t\] <- alp\[1\] * (c\[t\]==1) + alp\[2\]*(c\[t\]==2) + ph*x\[t-1\]install

- Download the latest version of Matlab

- Unzip the archive into a folder

- Add program folder to Matlab search path

addpath(path)

General settings

lightblue

lightred

% Seed the random number generator for repeatability

if eLan 'matlab', '7.2')

rnd('state', 0)

else

rng('default')

endLoad models and data

model parameter

tmax = 100; sig = .4;

Parse and compile BUGS model and sample data

model(file, data, 'sample', true); data = model;

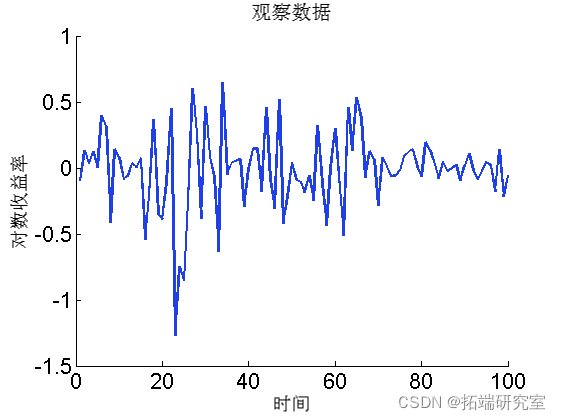

Draw data

figure('nae', 'Lrtrs')

plot(1:tmax, dt.y)

Biips sequence Monte Carlo SMC

Run SMC

n_part = 5000; % Particle number

{'x'}; % Variables to monitor

smc = samples(npart);

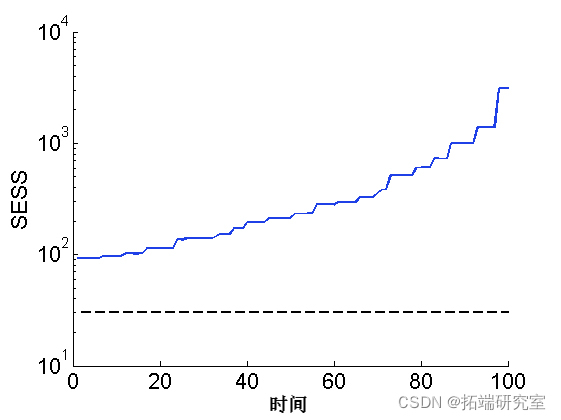

Algorithm diagnosis.

diag (smc);

Drawing smoothing ESS

sem(ess) plot(1:tmax, 30*(tmax,1), '--k')

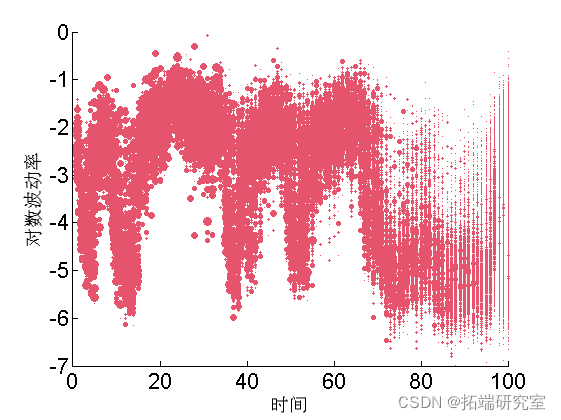

Paint weighted particles

for ttt=1:tttmax va = unique(outtt.x.s.vaues(ttt,:)); wegh = arrayfun(@(x) sum(outtt.x.s.weittt(ttt, outtt.x.s.vaues(ttt,:) == x)), va); scatttttter(ttt\*ones(size(va)), va, min(50, .5\*n_parttt*wegh), 'r',... 'markerf', 'r') end

Summary statistics

summary(out, 'pro', \[.025, .975\]);

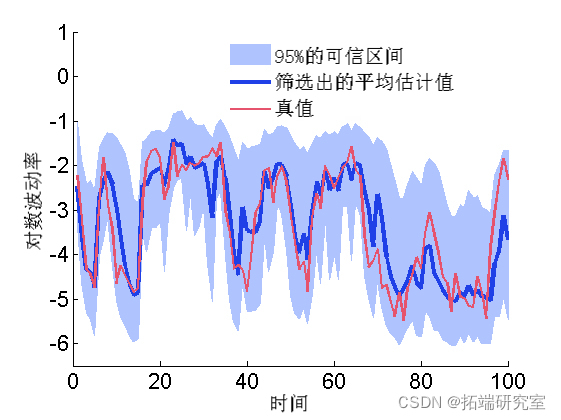

Mapping filter estimation

mean = susmc.x.f.mean;

xfqu = susmc.x.f.quant;

h = fill(\[1:tmax, tmax:-1:1\], \[xfqu{1}; flipud(xfqu{2})\], 0);

plot(1:tmax, mean,)

plot(1:tmax, data.x_true)

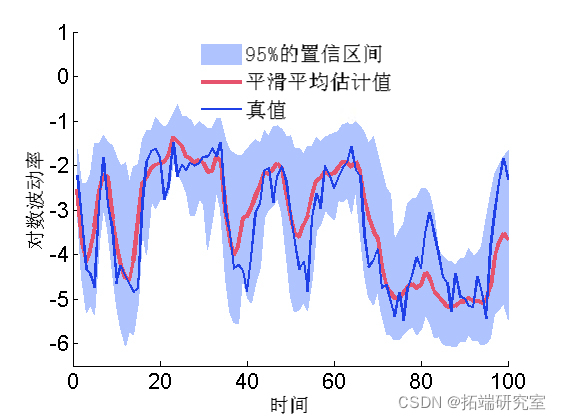

Mapping smoothing estimation

mean = smcx.s.mean; quant = smcx.s.quant; plot(1:t_max, mean, 3) plot(1:t\_max, data.x\_true, 'g')

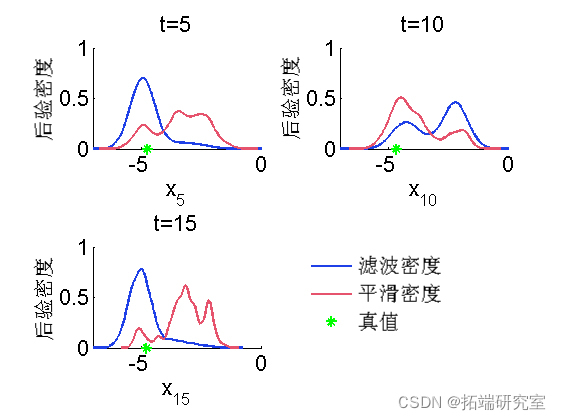

Marginal filtering and smoothing density

kde = density(out); for k=1:numel(time) tk = time(k); plot(kde.x.f(tk).x, kde.x.f(tk).f); hold on plot(kde.x.s(tk).x, kde.x.s(tk).f, 'r'); plot(data.xtrue(tk)); box off end

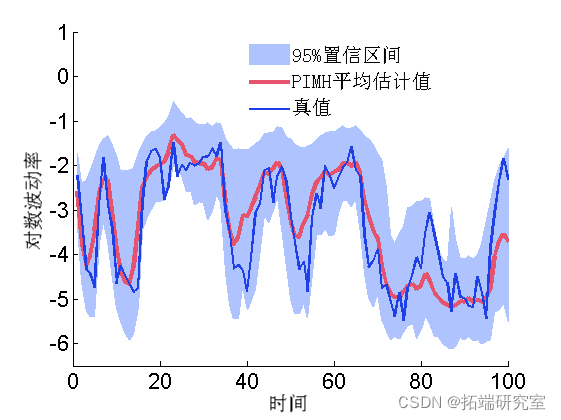

Biips particle independent metropolis Hastings

PIMH parameters

thi= 1; nprt = 50;

Running PIMH

init(moel, vaibls); upda(obj, urn, npat); % Pre burn iteration sample(obj,... nier, npat, 'thin', thn);

Some summary statistics

summary(out, 'prs');

Post mean and quantile

mean = sumx.man; quant = su.x.qunt; hold on plot(1:tax, man, 'r', 'liith', 3) plot(1:tax, xrue, 'g')

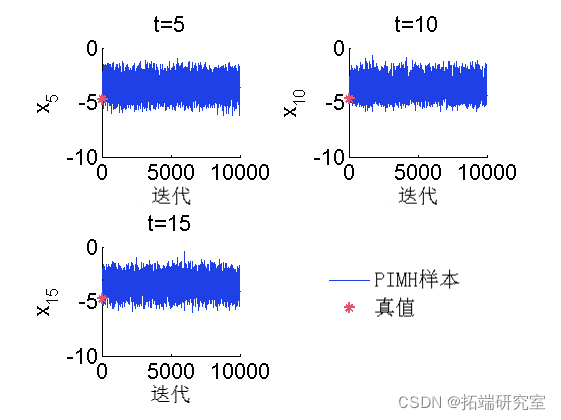

Trace of MCMC samples

for k=1:nmel(timndx) tk = tieinx(k); sublt(2, 2, k) plot(outm.x(tk, :), 'liedh', 1) hold on plot(0, d_retk), '*g'); box off end

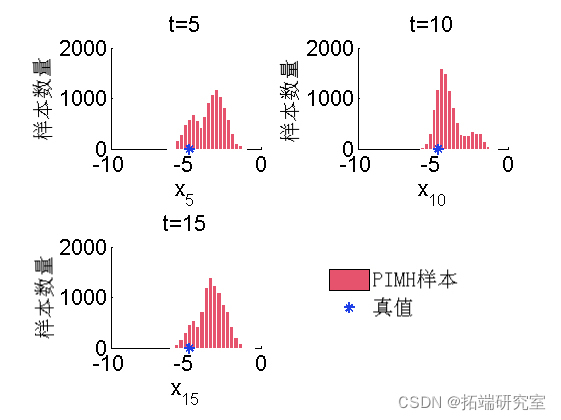

A posteriori histogram

for k=1:numel(tim_ix) tk = tim_ix(k); subplot(2, 2, k) hist(o_hx(tk, :), 20); h = fidobj(gca, 'ype, 'ptc'); hold on plot(daau(k), 0, '*g'); box off end

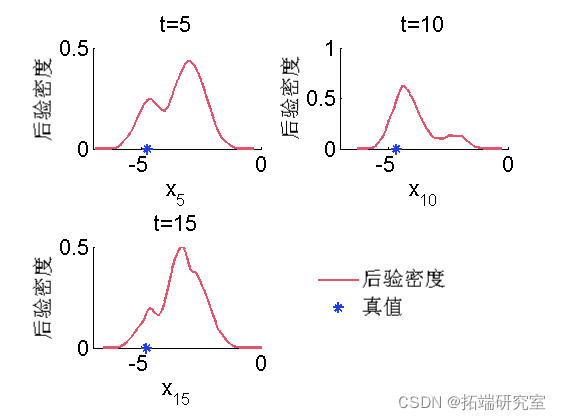

A posteriori kernel density estimation

pmh = desity(otmh); for k=1:numel(tenx) tk = tim_ix(k); subplot(2, 2, k) plot(x(t).x, dpi.x(tk).f, 'r'); hold on plot(xtrue(tk), 0, '*g'); box off end

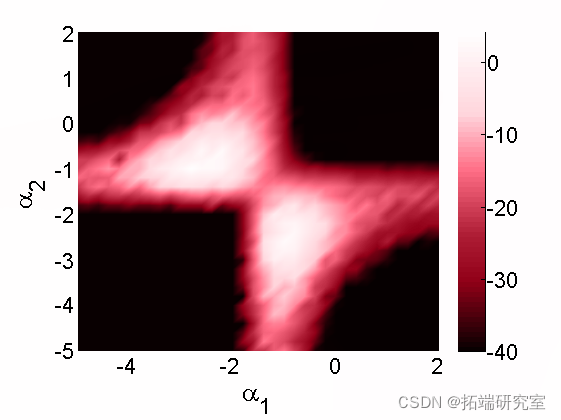

Biips sensitivity analysis

We want to study the sensitivity to parameter values

Algorithm parameters

n= 50; % Particle number

para = {'alpha}; % We want to study the parameters of sensitivity

% Value grid of two components

pvs = {A(:, B(:';Run sensitivity analysis using SMC

smcs(modl, par, parvlu, npt);

Plot log marginal likelihood and penalty log marginal likelihood rate

surf(A, B, reshape(ouma_i, sizeA) box off

Most popular insights

1.Simulation of hybrid queuing stochastic service queuing system with R language

2.Using queuing theory to predict waiting time in R language

3.Implementation of Markov chain Monte Carlo MCMC model in R language

4.Markov Regime Switching Model in R language Model ")

5.matlab Bayesian hidden Markov hmm model

6.Simulation of hybrid queuing stochastic service queuing system with R language

7.Python portfolio optimization based on particle swarm optimization

8.Research on traffic casualty accident prediction based on R language Markov transformation model