Home Credit Default Risk

conclusion

The data is provided by Home Credit (Chinese Name: Home Credit), which is dedicated to providing credit to people without bank accounts. The task requires forecasting whether the customer will repay the loan or encounter difficulties. AUC (ROC) is used as the evaluation standard of the model.

This blog only analyzes the application train / application test data, and uses Logistic Regression for classification and prediction. The results of public board 0.749 and private board 0.748 can be obtained by grid search. The Baseline is 0.68810, with a best score of 0.79857. The rest is in advanced level.

background knowledge

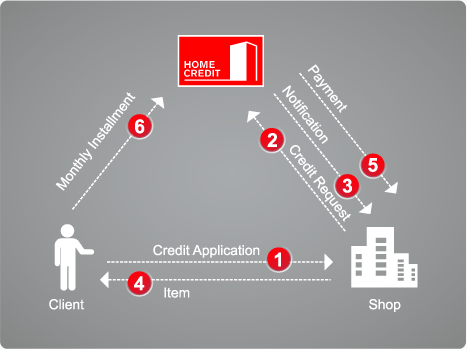

Home Credit is one of the leading consumer finance providers in central and Eastern Europe and Asia. It serves consumers in central and Eastern Europe (CEE), Russia, CIS and Asia.

Querying users' historical credit records in credit agencies can be used as a reference for risk assessment, but the credit data is often incomplete, because these people themselves have few bank records. The data set bureau.csv and bureau balance.csv correspond to this part of data.

There are three types of Home Credit products: credit card, POS (consumer loan) and cash loan. Credit cards are popular in Europe and the United States, but not in those countries. Therefore, the credit card data in the data set is less. POS can only buy things, cash loans can get cash. All three types of products have application and repayment records. In the data set, previous_application.csv, POS_CASH_BALANCE.csv, credit_card_balance.csv, installations_payment.csv correspond to this part of data.

The English versions of the three types of products are: Revolving loan (credit card), consumer installation loan (point of sales loan – POS loan), installation cash loan.

data set

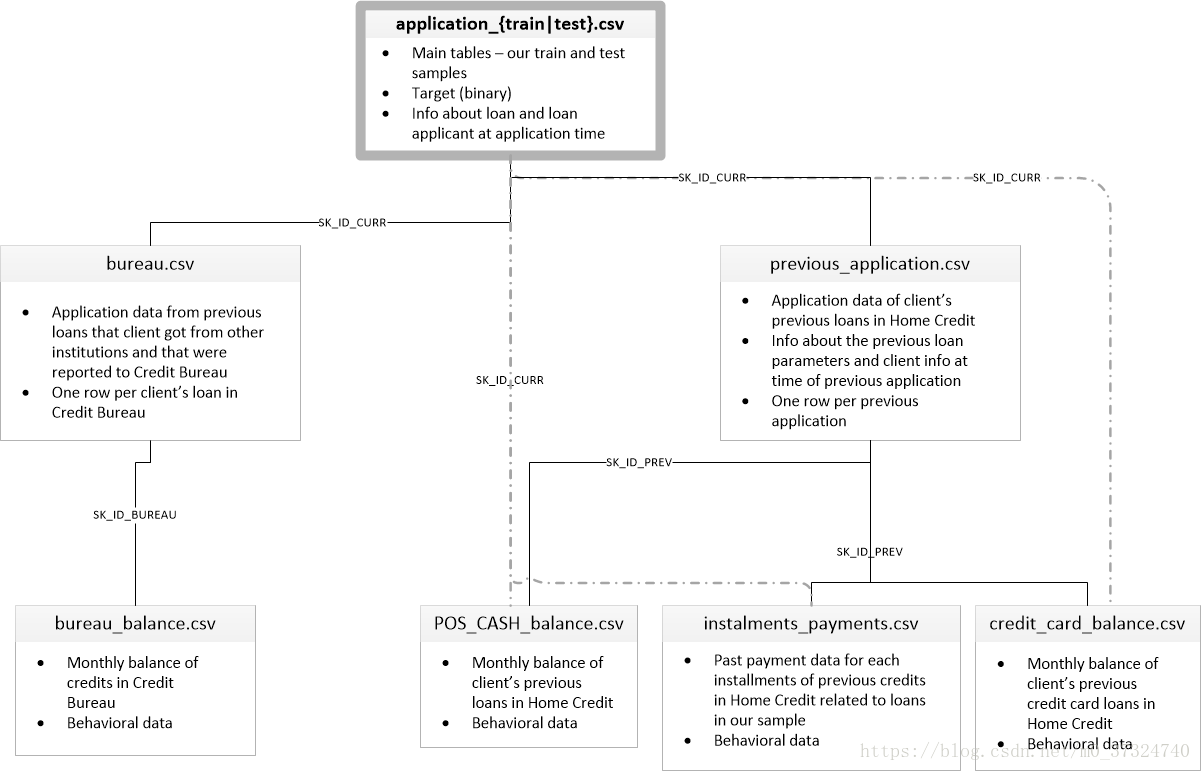

According to the introduction above, data set includes 8 different data files, which can be divided into three categories.

-

application_train, application_test:

The training set includes information about each loan application of Home Credit. Each loan has its own line and is identified by SK? ID? Curr. TARGET 0 of training set: the loan has been paid off, 1: the loan has not been paid off.

Through these two files, we can do basic data analysis and modeling for this task, which is also the content of this blog. -

bureau, bureau_balance:

These two documents are provided by credit agencies, the user's loan application data in other financial institutions, and the monthly repayment arrears record. A user (SK ﹣ ID ﹣ curr) can have multiple loan application data (SK ﹣ ID ﹣ Bureau). -

previous_application, POS_CASH_BALANCE,credit_card_balance,installments_payment

These four files are from Home Credit. Users may have used POS services, credit cards, and applied for loans at Home Credit. These documents are the relevant application data and repayment records. A user can have multiple historical data (SK ID prev).

The following figure shows how all the data are related, and links the three parts of data through three IDS, SK ﹣ ID ﹣ curr, SK ﹣ ID ﹣ Breau and SK ﹣ ID ﹣ prev.

Data analysis

Balance degree

Read data from application train and application test. There are 307511 data and 122 features in the training set. Among them, the number of defaults (Target = 1) is 24825, and the number of no defaults (Target = 0) is 282686. The imbalance is not serious.

# -*- coding: utf-8 -*- ##307511, 1220, 300000 data, 280000, 21000, this imbalance is not serious app_train = pd.read_csv('input/application_train.csv') app_test = pd.read_csv('input/application_test.csv') print('training data shape is', app_train.shape) print(app_train['TARGET'].value_counts())

training data shape is (307511, 122) 0 282686 1 24825 Name: TARGET, dtype: int64

Missing data

Of the 122 features, 67 were missing, of which 49 were missing more than 47%.

## 67 features are missing and 49 data are missing more than 47%. 47 of them are related to housing features. Can we use PCA to reduce this housing feature. See what others do with it. ## ext_source and own_car_age are left. Or these 49 features can be deleted. mv = app_train.isnull().sum().sort_values() mv = mv[mv>0] mv_rate = mv/len(app_train) mv_df = pd.DataFrame({'mv':mv, 'mv_rate':mv_rate}) print('number of features with more than 47% missing', len(mv_rate[mv_rate>0.47])) mv_rate[mv_rate> 0.47]

number of features with more than 47% missing 49 EMERGENCYSTATE_MODE 0.473983 TOTALAREA_MODE 0.482685 YEARS_BEGINEXPLUATATION_MODE 0.487810 YEARS_BEGINEXPLUATATION_AVG 0.487810 YEARS_BEGINEXPLUATATION_MEDI 0.487810 FLOORSMAX_AVG 0.497608 FLOORSMAX_MEDI 0.497608 FLOORSMAX_MODE 0.497608 HOUSETYPE_MODE 0.501761 LIVINGAREA_AVG 0.501933 LIVINGAREA_MODE 0.501933 LIVINGAREA_MEDI 0.501933 ENTRANCES_AVG 0.503488 ENTRANCES_MODE 0.503488 ENTRANCES_MEDI 0.503488 APARTMENTS_MEDI 0.507497 APARTMENTS_AVG 0.507497 APARTMENTS_MODE 0.507497 WALLSMATERIAL_MODE 0.508408 ELEVATORS_MEDI 0.532960 ELEVATORS_AVG 0.532960 ELEVATORS_MODE 0.532960 NONLIVINGAREA_MODE 0.551792 NONLIVINGAREA_AVG 0.551792 NONLIVINGAREA_MEDI 0.551792 EXT_SOURCE_1 0.563811 BASEMENTAREA_MODE 0.585160 BASEMENTAREA_AVG 0.585160 BASEMENTAREA_MEDI 0.585160 LANDAREA_MEDI 0.593767 LANDAREA_AVG 0.593767 LANDAREA_MODE 0.593767 OWN_CAR_AGE 0.659908 YEARS_BUILD_MODE 0.664978 YEARS_BUILD_AVG 0.664978 YEARS_BUILD_MEDI 0.664978 FLOORSMIN_AVG 0.678486 FLOORSMIN_MODE 0.678486 FLOORSMIN_MEDI 0.678486 LIVINGAPARTMENTS_AVG 0.683550 LIVINGAPARTMENTS_MODE 0.683550 LIVINGAPARTMENTS_MEDI 0.683550 FONDKAPREMONT_MODE 0.683862 NONLIVINGAPARTMENTS_AVG 0.694330 NONLIVINGAPARTMENTS_MEDI 0.694330 NONLIVINGAPARTMENTS_MODE 0.694330 COMMONAREA_MODE 0.698723 COMMONAREA_AVG 0.698723 COMMONAREA_MEDI 0.698723 dtype: float64

data type

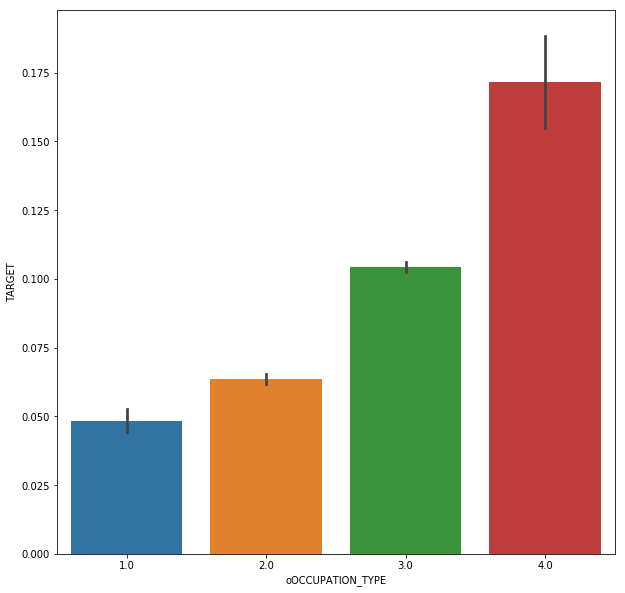

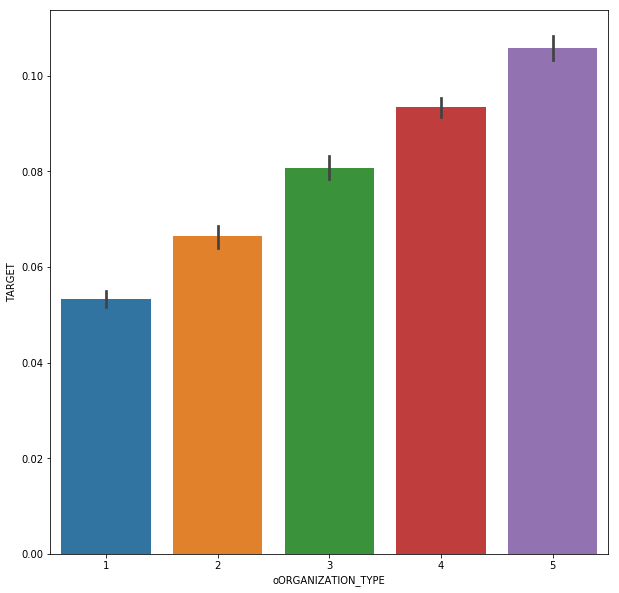

Of the 122 features, 65 are floating-point types, 41 are integer types, and 16 are non data features. The relationship between non data type feature and Target is analyzed. Occupation ﹣ type and organization ﹣ type can be manually coded, and the rest can be directly encoded by Onehot encoding.

## 65 floating-point, 41 integer, 16 non data features, except for location¢type and organization¢type, the rest should be able to be manually encoded categorical = [col for col in app_train.columns if app_train[col].dtypes == 'object'] ct = app_train[categorical].nunique().sort_values() for col in categorical: if (col!='OCCUPATION_TYPE') & (col!='ORGANIZATION_TYPE'): plt.figure(figsize = [10,10]) sns.barplot(y = app_train[col], x = app_train['TARGET']) # For the feature code with the feature number of 2, nunique is different from len(unique). The former does not calculate null, and the latter will calculate null

from sklearn.preprocessing import LabelEncoder lb = LabelEncoder() count = 0 for col in categorical: if len(app_train[col].unique()) == 2: count = count + 1 lb.fit(app_train[col]) app_train['o' + col] = lb.transform(app_train[col]) app_test['o' + col] = lb.transform(app_test[col]) # The overdue rate of housing type mode and family status is related to the classification. # OCCUPATION can be coded as follows col = 'OCCUPATION_TYPE' #occ_sort = app_train.groupby(['OCCUPATION_TYPE'])['TARGET'].agg(['mean','count']).sort_values(by = 'mean') #order1 = list(occ_sort.index) #plt.figure(figsize = [10,10]) #sns.barplot(y = app_train[col], x = app_train['TARGET'], order = order1) dict1 = {'Accountants' : 1, 'High skill tech staff':2, 'Managers':2, 'Core staff':2, 'HR staff' : 2,'IT staff': 2, 'Private service staff': 2, 'Medicine staff': 2, 'Secretaries': 2,'Realty agents': 2, 'Cleaning staff': 3, 'Sales staff': 3, 'Cooking staff': 3,'Laborers': 3, 'Security staff': 3, 'Waiters/barmen staff': 3,'Drivers': 3, 'Low-skill Laborers': 4} app_train['oOCCUPATION_TYPE'] = app_train['OCCUPATION_TYPE'].map(dict1) app_test['oOCCUPATION_TYPE'] = app_test['OCCUPATION_TYPE'].map(dict1) plt.figure(figsize = [10,10]) sns.barplot(x = app_train['oOCCUPATION_TYPE'], y = app_train['TARGET']) ## col = 'ORGANIZATION_TYPE' #organ_sort = app_train.groupby(['ORGANIZATION_TYPE'])['TARGET'].agg(['mean','count']).sort_values(by = 'mean') #order1 = list(organ_sort.index) #plt.figure(figsize = [20,20]) #sns.barplot(y = app_train[col], x = app_train['TARGET'], order = order1) dict1 = {'Trade: type 4' :1, 'Industry: type 12' :1, 'Transport: type 1' :1, 'Trade: type 6' :1, 'Security Ministries' :1, 'University' :1, 'Police' :1, 'Military' :1, 'Bank' :1, 'XNA' :1, 'Culture' :2, 'Insurance' :2, 'Religion' :2, 'School' :2, 'Trade: type 5' :2, 'Hotel' :2, 'Industry: type 10' :2, 'Medicine' :2, 'Services' :2, 'Electricity' :2, 'Industry: type 9' :2, 'Industry: type 5' :2, 'Government' :2, 'Trade: type 2' :2, 'Kindergarten' :2, 'Emergency' :2, 'Industry: type 6' :2, 'Industry: type 2' :2, 'Telecom' :2, 'Other' :3, 'Transport: type 2' :3, 'Legal Services' :3, 'Housing' :3, 'Industry: type 7' :3, 'Business Entity Type 1' :3, 'Advertising' :3, 'Postal':3, 'Business Entity Type 2' :3, 'Industry: type 11' :3, 'Trade: type 1' :3, 'Mobile' :3, 'Transport: type 4' :4, 'Business Entity Type 3' :4, 'Trade: type 7' :4, 'Security' :4, 'Industry: type 4' :4, 'Self-employed' :5, 'Trade: type 3' :5, 'Agriculture' :5, 'Realtor' :5, 'Industry: type 3' :5, 'Industry: type 1' :5, 'Cleaning' :5, 'Construction' :5, 'Restaurant' :5, 'Industry: type 8' :5, 'Industry: type 13' :5, 'Transport: type 3' :5} app_train['oORGANIZATION_TYPE'] = app_train['ORGANIZATION_TYPE'].map(dict1) app_test['oORGANIZATION_TYPE'] = app_test['ORGANIZATION_TYPE'].map(dict1) plt.figure(figsize = [10,10]) sns.barplot(x = app_train['oORGANIZATION_TYPE'], y = app_train['TARGET']) ## The rest of them are ohe(307511, 127),(48744, 126) drop, and the feature s are 122121 discard_features = ['ORGANIZATION_TYPE', 'OCCUPATION_TYPE','FLAG_OWN_CAR','FLAG_OWN_REALTY','NAME_CONTRACT_TYPE'] app_train.drop(discard_features,axis = 1, inplace = True) app_test.drop(discard_features,axis = 1, inplace = True) # Then use get Dummies (307511, 169) (48744, 165) app_train = pd.get_dummies(app_train) app_test = pd.get_dummies(app_test) print('Training Features shape: ', app_train.shape) print('Testing Features shape: ', app_test.shape) # Some features are not included in the test and need to be aligned (307511, 166) (48744, 165) train_labels = app_train['TARGET'] app_train, app_test = app_train.align(app_test, join = 'inner', axis = 1) app_train['TARGET'] = train_labels print('Training Features shape: ', app_train.shape) print('Testing Features shape: ', app_test.shape)

Training Features shape: (307511, 169) Testing Features shape: (48744, 165) Training Features shape: (307511, 166) Testing Features shape: (48744, 165)

Outliers

Abnormal data is found in the feature days employee, which has a strong correlation with Target and needs special processing. In addition, add a feature, days? Employee? Anom, to indicate whether the feature is abnormal. This processing should be more effective for linear methods, and tree based methods should be able to identify automatically.

## Continue to EDA, and find the problem data in the days employee. This processing should be effective for the linear method, and the boost method should be able to identify automatically. app_train['DAYS_EMPLOYED'].plot.hist(title = 'DAYS_EMPLOYMENT HISTOGRAM') app_test['DAYS_EMPLOYED'].plot.hist(title = 'DAYS_EMPLOYMENT HISTOGRAM') app_train['DAYS_EMPLOYED_ANOM'] = app_train['DAYS_EMPLOYED'] == 365243 app_train['DAYS_EMPLOYED'].replace({365243: np.nan}, inplace = True) app_test['DAYS_EMPLOYED_ANOM'] = app_test["DAYS_EMPLOYED"] == 365243 app_test["DAYS_EMPLOYED"].replace({365243: np.nan}, inplace = True) app_train['DAYS_EMPLOYED'].plot.hist(title = 'Days Employment Histogram'); plt.xlabel('Days Employment') ## Extract correlation correlations = app_train.corr()['TARGET'].sort_values() print('Most Positive Correlations:\n', correlations.tail(15)) print('\nMost Negative Correlations:\n', correlations.head(15))

Most Positive Correlations: REG_CITY_NOT_LIVE_CITY 0.044395 FLAG_EMP_PHONE 0.045982 NAME_EDUCATION_TYPE_Secondary / secondary special 0.049824 REG_CITY_NOT_WORK_CITY 0.050994 DAYS_ID_PUBLISH 0.051457 CODE_GENDER_M 0.054713 DAYS_LAST_PHONE_CHANGE 0.055218 NAME_INCOME_TYPE_Working 0.057481 REGION_RATING_CLIENT 0.058899 REGION_RATING_CLIENT_W_CITY 0.060893 oORGANIZATION_TYPE 0.070121 DAYS_EMPLOYED 0.074958 oOCCUPATION_TYPE 0.077514 DAYS_BIRTH 0.078239 TARGET 1.000000 Name: TARGET, dtype: float64 Most Negative Correlations: EXT_SOURCE_3 -0.178919 EXT_SOURCE_2 -0.160472 EXT_SOURCE_1 -0.155317 NAME_EDUCATION_TYPE_Higher education -0.056593 CODE_GENDER_F -0.054704 NAME_INCOME_TYPE_Pensioner -0.046209 DAYS_EMPLOYED_ANOM -0.045987 FLOORSMAX_AVG -0.044003 FLOORSMAX_MEDI -0.043768 FLOORSMAX_MODE -0.043226 EMERGENCYSTATE_MODE_No -0.042201 HOUSETYPE_MODE_block of flats -0.040594 AMT_GOODS_PRICE -0.039645 REGION_POPULATION_RELATIVE -0.037227 ELEVATORS_AVG -0.034199 Name: TARGET, dtype: float64

Fill in missing values

## Feature Engineering ## Fill in missing values from sklearn.preprocessing import Imputer, MinMaxScaler imputer = Imputer(strategy = 'median') scaler = MinMaxScaler(feature_range = [0,1]) train = app_train.drop(columns = ['TARGET']) imputer.fit(train) train = imputer.transform(train) test = imputer.transform(app_test) scaler.fit(train) train = scaler.transform(train) test = scaler.transform(test) print('Training data shape: ', train.shape) print('Testing data shape: ', test.shape)

D:\Anaconda3\lib\site-packages\sklearn\utils\deprecation.py:66: DeprecationWarning: Class Imputer is deprecated; Imputer was deprecated in version 0.20 and will be removed in 0.22. Import impute.SimpleImputer from sklearn instead. warnings.warn(msg, category=DeprecationWarning) Training data shape: (307511, 166) Testing data shape: (48744, 166)

modeling

Logistic Regression

The results show that when 'C' = 1 and 'Penalty' = 'l1', the performance is the best.

## from sklearn.linear_model import LogisticRegression from sklearn.model_selection import GridSearchCV param_grid = {'C' : [0.01,0.1,1,10,100], 'penalty' : ['l1','l2']} log_reg = LogisticRegression() grid_search = GridSearchCV(log_reg, param_grid, scoring = 'roc_auc', cv = 5) grid_search.fit(train, train_labels) # Train on the training data log_reg_best = grid_search.best_estimator_ log_reg_pred = log_reg_best.predict_proba(test)[:, 1] submit = app_test[['SK_ID_CURR']] submit['TARGET'] = log_reg_pred submit.head() submit.to_csv('log_reg_baseline_gridsearch2.csv', index = False)

The final result public board 0.73889 private board 0.73469

LightGBM

folds = KFold(n_splits= num_folds, shuffle=True, random_state=1001) # Create arrays and dataframes to store results oof_preds = np.zeros(train_df.shape[0]) sub_preds = np.zeros(test_df.shape[0]) feature_importance_df = pd.DataFrame() feats = [f for f in train_df.columns if f not in ['TARGET','SK_ID_CURR','SK_ID_BUREAU','SK_ID_PREV','index']] for n_fold, (train_idx, valid_idx) in enumerate(folds.split(train_df[feats], train_df['TARGET'])): train_x, train_y = train_df[feats].iloc[train_idx], train_df['TARGET'].iloc[train_idx] valid_x, valid_y = train_df[feats].iloc[valid_idx], train_df['TARGET'].iloc[valid_idx] # LightGBM parameters found by Bayesian optimization clf = LGBMClassifier( nthread=4, n_estimators=10000, learning_rate=0.02, num_leaves=34, colsample_bytree=0.9497036, subsample=0.8715623, max_depth=8, reg_alpha=0.041545473, reg_lambda=0.0735294, min_split_gain=0.0222415, min_child_weight=39.3259775, silent=-1, verbose=-1, ) clf.fit(train_x, train_y, eval_set=[(train_x, train_y), (valid_x, valid_y)], eval_metric= 'auc', verbose= 200, early_stopping_rounds= 200) oof_preds[valid_idx] = clf.predict_proba(valid_x, num_iteration=clf.best_iteration_)[:, 1] sub_preds += clf.predict_proba(test_df[feats], num_iteration=clf.best_iteration_)[:, 1] / folds.n_splits fold_importance_df = pd.DataFrame() fold_importance_df["feature"] = feats fold_importance_df["importance"] = clf.feature_importances_ fold_importance_df["fold"] = n_fold + 1 feature_importance_df = pd.concat([feature_importance_df, fold_importance_df], axis=0) print('Fold %2d AUC : %.6f' % (n_fold + 1, roc_auc_score(valid_y, oof_preds[valid_idx]))) del clf, train_x, train_y, valid_x, valid_y gc.collect() print('Full AUC score %.6f' % roc_auc_score(train_df['TARGET'], oof_preds))

private board 0.74847 public board0.74981

Feature importance

Appendix: meaning of each field

| field | Meaning |

|---|---|

| SK_ID_CURR | ID of this application |

| TARGET | Repayment risk of the applicant: 1-high risk; 0-low risk |

| NAME_CONTRACT_TYPE | Loan type: cash or revolving |

| CODE_GENDER | Applicant gender |

| FLAG_OWN_CAR | Does the applicant have a car |

| FLAG_OWN_REALTY | Does the applicant have a room |

| CNT_CHILDREN | Number of children of applicant |

| AMT_INCOME_TOTAL | Income status of applicants |

| AMT_CREDIT | Loan amount applied for this time |

| AMT_ANNUITY | Loan annuity |

| AMT_GOODS_PRICE | If it is a consumer loan, change the field to represent the actual price of the goods |

| NAME_TYPE_SUITE | Accompanying personnel of the applicant for this application |

| NAME_INCOME_TYPE | Type of applicant's income |

| NAME_EDUCATION_TYPE | Education level of applicant |

| NAME_FAMILY_STATUS | Applicant's marital status |

| NAME_HOUSING_TYPE | Living conditions of the applicant (rented house, purchased house, lived with parents, etc.) |

| REGION_POPULATION_RELATIVE | Population density of applicant's residence, standardized |

| DAYS_BIRTH | Applicant's date of birth (days from the date of application, negative) |

| DAYS_EMPLOYED | Working years of the applicant (days from the date of application, negative) |

| DAYS_REGISTRATION | The time when the applicant last modified the registration information (days from the date of application, negative value) |

| DAYS_ID_PUBLISH | The time when the applicant last modified the identity document of the loan application (days from the date of application, negative value) |

| FLAG_MOBIL | Does the applicant provide personal phone number (1-yes, 0-no) |

| FLAG_EMP_PHONE | Does the applicant provide home phone (1-yes, 0-no) |

| FLAG_WORK_PHONE | Does the applicant provide a work phone number (1-yes, 0-no) |

| FLAG_CONT_MOBILE | Whether the personal phone of the applicant can be dialed (1-yes, 0-no) |

| FLAG_EMAIL | Whether the applicant provides email (1-yes, 0-no) |

| OCCUPATION_TYPE | Position of applicant |

| REGION_RATING_CLIENT | The company's rating of the applicant's residential area (1, 2, 3) |

| REGION_RATING_CLIENT_W_CITY | In consideration of the city, the company's rating of the applicant's residential area (1,2,3) |

| WEEKDAY_APPR_PROCESS_START | What day of the week is the applicant initiating the application |

| HOUR_APPR_PROCESS_START | The hour the applicant initiated the application |

| REG_REGION_NOT_LIVE_REGION | Whether the permanent address and contact address provided by the applicant match (1-do not match, 2-match, regional level) |

| REG_REGION_NOT_WORK_REGION | Whether the permanent address and working address provided by the applicant match (1-mismatch, 2-match, region level) |

| LIVE_REGION_NOT_WORK_REGION | Whether the contact address and working address provided by the applicant match (1-do not match, 2-match, regional level) |

| REG_CITY_NOT_LIVE_CITY | Whether the permanent address and contact address provided by the applicant match (1-do not match, 2-match, city level) |

| REG_CITY_NOT_WORK_CITY | Whether the permanent address and working address provided by the applicant match (1-do not match, 2-match, city level) |

| LIVE_CITY_NOT_WORK_CITY | Whether the contact address and work address provided by the applicant match (1-do not match, 2-match, city level) |

| ORGANIZATION_TYPE | Organization type of applicant |

| EXT_SOURCE_1 | Standardized scoring of external data source 1 |

| EXT_SOURCE_2 | Standardized scoring of external data source 2 |

| EXT_SOURCE_3 | Standardized scoring of external data source 3 |

| APARTMENTS_AVG <----> EMERGENCYSTATE_MODE | Standardized scores of various indicators of the applicant's living environment |

| OBS_30_CNT_SOCIAL_CIRC LE <----> DEF_60_CNT_SOCIAL_CIRCLE | The meaning of these fields is not understood |

| DAYS_LAST_PHONE_CHANGE | Time when the applicant last modified the mobile phone number (days from the date of application, negative value) |

| FLAG_DOCUMENT_2 <----> FLAG_DOCUMENT_21 | Does the applicant provide additional documents 2, 3, 4.21 |

| AMT_REQ_CREDIT_BUREAU_HOUR | The number of times the applicant has been inquired about the credit investigation within 1 hour before the application is initiated |

| AMT_REQ_CREDIT_BUREAU_DAY | The number of times the applicant has been inquired about the credit investigation within one day before the application is initiated |

| AMT_REQ_CREDIT_BUREAU_WEEK | The number of times the applicant has been inquired about the credit investigation within one week before the application is initiated |

| AMT_REQ_CREDIT_BUREAU_MONTH | The number of times the applicant has been inquired about the credit investigation within one month before the application is initiated |

| AMT_REQ_CREDIT_BUREAU_QRT | The number of times the applicant has been inquired about the credit investigation within one quarter before the application is initiated |

| AMT_REQ_CREDIT_BUREAU_YEAR | The number of times the applicant has been inquired about the credit investigation within one year before the application is initiated |

From the table, we can roughly guess some information, such as: location, name, ncome and organization types should have strong linear correlation; days, last, phone, change, hour, appr, process, start and other information may not be important features; they can be verified in later feature analysis and take specific dimension reduction measures